Sankalp's Monthly Macro Views - Oct 2022 #8

Sankalp's Monthly Macro Views - Oct 2022 #8

Q4 outlook, FED pivot, trouble in Fx markets, crypto DCA list

DISCLAIMER: Nothing in this post is financial advise. Certain information in this post, including, statements regarding Rising Capital and its associated companies, (collectively “Rising”) anticipated business, investments or opportunities, may constitute forward looking information. Because of various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking information. These are authors’ personal views and should not form the basis for making investment decisions, or be considered a recommendation or advice to engage in investment transactions.

"When the time comes to buy, you won't want to."

-Wally Deemer

I was at the Token2049 conference in Singapore a couple of weeks ago. Huge crowds of dedicated builders, enthusiasts, investors, founders, 8000+ people, 25+ booths, numerous daily side events, hackathons etc, and as usual some crazy parties. My takeaways:

This does not feel like a 2016 or 2018/19 bear market at all. No one is quitting this time around. Rather, builders are building. BUIDL for the next 12 months, and reap rewards in the next bull market.

Hats off to Singapore for conducting not just the largest crypto asset week, but several other parallel events including the much coveted F1. Clearly, it has established itself as the crypto hub of Asia. However, talent is getting hard to find and remains very expensive.

There is a lot of capital available for brilliant founders. VC Funds continue to raise 10’s and 100’s of millions more to deploy further.

Crypto’s time as an independent asset class, has come. A hige future awaits for builders building now.

1. TL;DR

September was once again gloom and doom for all markets, just like August before that. BTC & ETH were no exceptions.

The FED tightening continues as tighter financial conditions are unable to slow the economy YET. However, there are signs of reversals as Inflation seems to have peaked, international markets are stretched (bonds, Fx, UK, Japan), DXY seems to have paused its rally for now, 2Y/10Y bond yield reversals point to a recession in 2023, housing seems to be cooling and jobs / wages could follow. CPI & wage growth numbers are the two key metrics everyone is watching. FED will respond accordingly. My base case is a 75bps hike in November, 50bps in December and 25 bps in January. The market is forward looking however, and we could see some relief rallies beginning in October itself. I still don’t see FED pivoting (easing) unless something breaks in the domestic markets in Q1.

An almost collapse of the UK Gilt markets till BoE Intervened with GBP 65bn. With this intervention, BoE has embarked on a path that they cannot return from. BoJ took a similar path 20 years ago and again intervened last month in Fx markets to save their collapsing currency. This is YCC (Yield Curve Control) - basically preventing bond yields from exploding so that other parts of the economy do not explode with it. The EU & China, and other indebted nations will follow as their debts become unsustainable. Bureaucrats must be back channeling with the US to stop tightening - and the US might have to oblige with a pause or pivot in Q1.

This positions us for a relief rally shorter term, but broader economic conditions remain in the gutter for medium to longer term. Too many uncertainties and too much debt that is very difficult to get out of. I believe that the central banks might have lost control and all roads lead to some sort of tragedy in the medium to long term - war, civil riots, hyperinflation (especially food). That is the only way for governments to distract its citizens and blame their past mess on something or someone that does not concern them directly. Dollar is taking a breather which could also mean more allocation to risk assets including crypto. But these are just the first signs. We continue to watch closely.

The Nord Stream pipeline was blown up by miscreants. This makes a bad gas situation even worse for Europe. We wrote in more detail here last month. A severe winter and rising inflation in Europe could have dire consequences on demand. That could stall economic activity which could in turn drive EU to recession. Moreover, with different economic & geopolitical agendas, EU seems poised to YCC. That does not bore well for Euro.

Several other moving macro parts could derail our base thesis above including escalating gas prices, civil unrest in developed and emerging markets, further war escalation in Europe, food inflation leading into Christmas celebrations, inverted US treasury yields, falling currencies, US treasury sales by its holders etc. Each one of these can pop its ugly head anytime. It is very difficult to time these or to know the severity of destruction in advance. While you start to see signs of pause / pivot by FED, keep an eye on these macro indicators.

Overall, everyone is utterly pessimistic. Investors are pricing in recessions but markets are notorious for relief rallies that can sustain for a long period of time. I wouldn’t be surprised to see some if market starts to get hints of a FED slow down, pause or a pivot in rate hikes - directly or indirectly like the repo rates that have already been deployed since the first week of October.

👇big drop in reverse repos - driving up $ liquidity. Aka indirect QE. Is FED worried what happened in UK gilts/Yen or is something broken in private credit markets? FED seems worried. This was post emergency meeting. More liquidity = risk on. Early to say thanks @CryptoHayes https://t.co/XzV0Hyo6UM1/ Curious thangs going on with $ liq

👇big drop in reverse repos - driving up $ liquidity. Aka indirect QE. Is FED worried what happened in UK gilts/Yen or is something broken in private credit markets? FED seems worried. This was post emergency meeting. More liquidity = risk on. Early to say thanks @CryptoHayes https://t.co/XzV0Hyo6UM1/ Curious thangs going on with $ liq Arthur Hayes @CryptoHayes

Arthur Hayes @CryptoHayesGiven above global macro, crypto’s correlation to macro, monthly flows on-chain, ETH merge narrative pass us, and BTC halving narrative still far away, I believe we stay range bound just like we said last month:

Bottomline - Smart money is accumulating and providing a floor for now. Any macro improvements could lead to a relief rally into October / November but capped by global uncertainties. Unless global macro improves or something breaks AND FED is back to printing, these rallies have limited steam.

I am watching some alt coins and levels very closely including ETH (that I am very bullish on at these price levels), cash flow coins (UNI, SUSHI, GMX, AAVE, BNB, FTT), OG protocol coins (SOL, Matic, BNB again) and some riskier bets as explained below.

Bottomline here is that FED could signal a pause, if not a pivot, for good or bad reasons. If you saved some moolah from the last cycle or if have a consistent source of income, then this is the time to start dipping your toes and backing up the rest of your cash trucks. Fortune favours the brave. You will never get some of these opportunities ever again - whether you are a builder, an investor, long term holder, or perhaps even new to crypto. It can surely get worse, but always weigh your existing portfolio, your cash flow positions and risk vs reward for every investment or give it to a manager that lives by it.

2. Macro Conundrum

After a moribund September, I am trying to resolve a very simple conundrum this month in my mind:

Is something about to break or get so bad that central banks and governments will pause their rate hiking and resort back to direct or indirect QE?

Or have they gone so far in their debt expeditions that they have lost control and things are about to get very ugly?

The answer that I have found is - TIMING. I believe in the short term (3-6 months), we go back to some sort of pause or pivot again (read QE) and try to kick the can further BUT in the medium to longer term, things are about to get a bit ugly with sustained inflation and numerous uncertain geopolitical situations. Let’s explore together how I got there and where are the opportunities.

3. FED pause or a forced pivot? Getting closer.

FED continues to tighten with sticky inflation and a hot economy: With inflation still sticky at 8.3% and a very healthy jobs market, FED will continue to tighten in the short term. With looming mid-November elections, our base case is that FED will hike by 75bps in November, 50 bps in December and 25 bps in January as:

Pressure starts to mount up from other central bankers

Economy starts to cool and tightening starts to take its intended effect

That means there is still pain in the markets for now but that pain is already priced in. The market is forward looking in its outlook. If CPI prints around 8% or lower, we might see a brief rally into the month end. Good news is that Inflation seems to have peaked for now but we are yet to see other economic activities to subside. Powell has been very clear - inflation needs to come down and they will use any tool necessary. Market is anticipating a lower CPI print, and starting to rally in first October - perhaps buy the rumour, sell the news. If inflation is tamed, the rallies in crypto might be relatively larger, but with a cap.

S&P is back to June lows but not enough pain yet: S&P had a decent relief rally in August but is back to “just” June lows for now. That is to say there is much more room before something breaks in the equity markets. Perhaps another 10-20% downside from here? With first signs of FED pivot (due to lower CPI nos. and lower wage growth), we could see a relief rally in equities sooner than everyone is anticipating.

US Housing is declining but not at alarming levels yet for FED to consider a pause. That should change by November because:

The US housing market is seeing a reversal with new housing stats declining by 15% plus but we are not there yet.

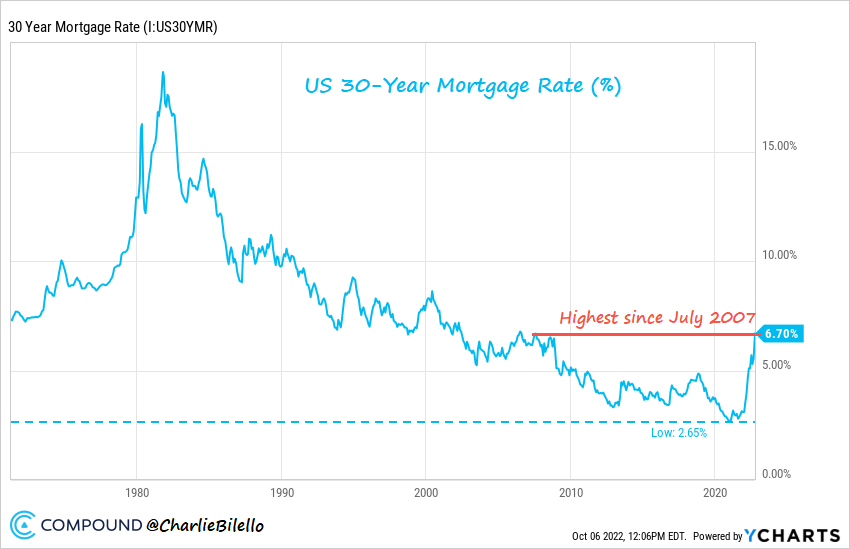

Mortgage demand is declining in line with increasing mortgage rates, almost 30% YTD at some places.

UK and Europe housing is starting to see declines as well

But global markets like Singapore and Dubai are getting so out of control that governments have had to announce cooling measures.

The FED’s last purchase of MBS (mortgage backed securities) will settle on October 20th, 2022. What after this? How much MBS will FED sell? Will they sell at all? There will be some negative headlines. Be prepared as housing starts to fall steeply after November. They have timed this very well, just after the elections to avoid a double whammy of inflation as well as housing. This increases the chances of a FED pause even more.

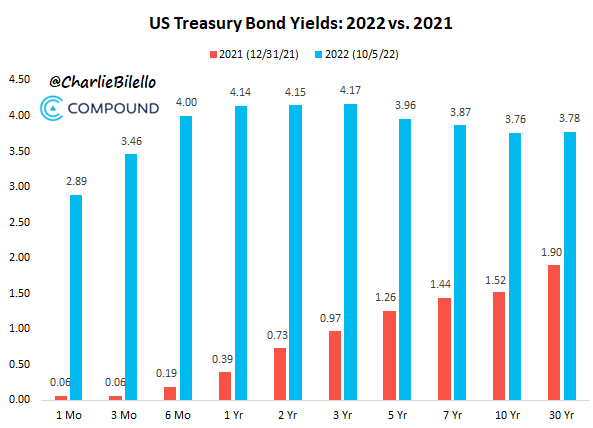

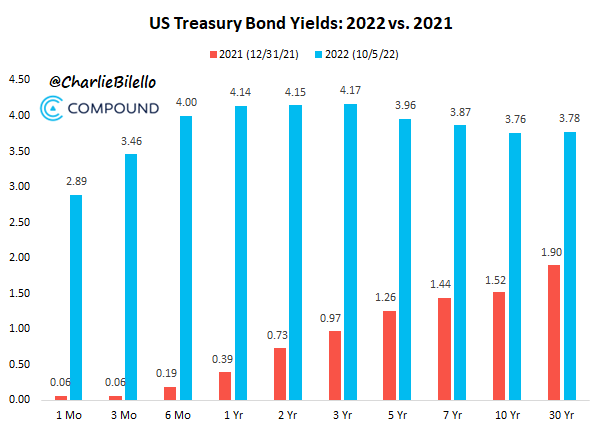

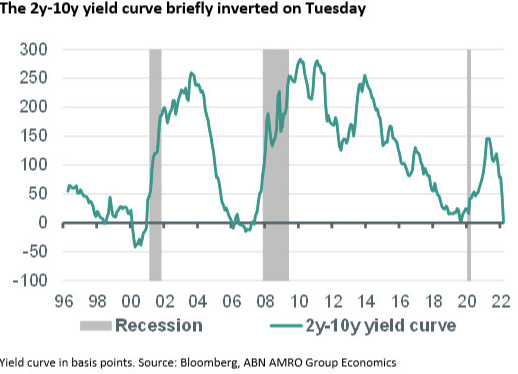

US Inverted Bond Yields usually indicate recessions but with a lag: When 2Y short term > 10Y bonds, usually it means something is broken. Basically, someone is willing to offer you more return in the short term as they are worried about long term growth. 2Y/10Y is inverted now but that does not indicate immediate recession. While yield curve inversion has been a leading indicator of recession, it has to sustain for a month and usually there is a lag of 6-12 months for a recession to follow. The market is saying that rates will be cut at some point in 6-12 months as recession cuts demand.

Healthy job market but signs of layoffs and wage tightening starting to appear: The US jobs report shows that employment is steaming at a healthy speed. Not just the US, there is a healthy demand for talent globally, albeit layoffs have started to emerge here and there. Until such time that unemployment stays low, FED has no upside to start pausing or cutting rates again.

4. Developed market currency crisis

UK Gilts collapsed & BoE intervened - What’s next? In the last week of September, we saw UK 10Y Gilts yields jumped from around 3.5% to around 5% on the back of some short sellers that did not like unlimited fiscal mini budget presented by the new government. BoE had to intervene, announcing unlimited purchases just like their European counterpart a few years ago. They had no choice. Their only other choice was a painful and sudden collapse of UK pension funds that were being margin called for their over leveraged positions in Liability Driven Investment funds. GBP 65bn was pumped to save the day. This is indirect QE. More importantly this is a path from which BoE cannot return and leads to yield caps and controls. Aka printing. Aka inflation and pain.

I am going to try to explain why the Bank of England has gone into the market to buy up to £65bn of UK government bonds with maturities of 20 years or more, including £1bn today. It all stems from a dramatic collapse in the price of these government bonds, called gilts, a...

I am going to try to explain why the Bank of England has gone into the market to buy up to £65bn of UK government bonds with maturities of 20 years or more, including £1bn today. It all stems from a dramatic collapse in the price of these government bonds, called gilts, a...While BoE was able to save face in the short term, in the long term it has set itself against markets forces that will force it to adopt YCC. That is to say that both the EU as well as BoE have lost control. What is amazing to see is that emerging markets in Asia are holding relatively ok so far. A look at the chart below and you see that it’s the developed markets that are heavily indebted this time around. How much longer can they kick the can further down the road? It is not a matter of if, but when.

On the currency side, it hasn't been any better with corporate and wealthy clients holding GBP in their banks getting worried. There could be an exodus to USD at some point. Or perhaps some to Gold & BTC. For the layman, monthly energy bills and monthly mortgage payments are hurting. Most of the UK's borrowers are on floating rate mortgages that have jumped more than 50% in the last 3 months. Things are about to get worse as UK prints more and moves towards YCC. That is all very negative for the GBP vs the dollar or Gold or BTC.

BoJ intervention has got the FED worried as they are one of the largest US Treasuries holders: BoJ had no choice but to intervene as Yen continued to drop against the USD, creating havoc for importers there. BoJ sold around $20bn USD for Yen. They are also one of the largest holders of US Treasuries. Next they could be selling US treasuries. The US does not want to open that Pandora’s box where every other nation starts to sell treasuries. That will be worse than any war. US Treasury sales = US Treasury prices drop = Yields go up = Debt payments for governments and corporate go bonkers = forward looking cash models start discounting even more = earnings are hit and markets crash. This would also create a cascade of dollar redemptions that FED can never meet. We believe that such a situation will not occur. The FED & its counterparts will pause much before that. Kicking the can down the road is a much better option for politicians and their central bank lieutenants. Back to printer please.

The Unknown keep me awake - black swans circling the economic skies

Many unexpected events in September could be a precursor to several other black swan events including:

The Nord Stream pipeline was sabotaged. There are better pundits than I who can point the finger on who is behind that. But this sets the stage for an already bad situation to become worse in European gas saga that we covered last month here. Storage is getting better and demand is declining. That means recession starts to become real. Just like BoJ & BoE, Europeans are printing unlimited, non-stop. They call it Energy subsidies. The UK calls it Gilt protection. Japan calls it currency protection. Inflation continues unabated and if the printer is running non stop, we could easily see a run on currencies and bonds again. Higher inflation and a real food crisis is not ruled out for Europe. That is all very negative for the Euro vs the dollar or Gold or BTC.

Russia is escalating its war in Ukraine by calling in more troops and threatening nuclear action. But is that threat real? There is no one better than Mikhail Khodorkovskywho was imprisoned for 10 years and was once the richest man in Russia. He recommends the west to take it seriously as Putin has his credibility and perhaps his life at stake. If that swan was to fly, then all bets are off and the world is truly s****d.

5. CRYPTO NARRATIVE

We are macro investors focussed on medium-long term projects and coins. Just like broader macro, crypto had its’ own share of action filled drama in September. While correlation to macro is driving the general direction, that correlation is starting to weaken a bit. Very early to say, and crypto could still get very ugly with how macro “misbehaves” from here. We wrote about that in our last months’ September Macro Monthly:

Bottomline: A quick look into August and what has prevailed in September so far, one can clearly see stress everywhere - financial stress, war stress, geopolitical stress, civil unrest stress. The macro scenario is ugly to say the least. In the short term, there are a lot of moving parts. There is hardly anything to be bullish about.

Crypto Thesis - Q4 should be better

Everyone expected crypto to hit lows like equities. However, this resilience in Sept was welcoming but we are far from decoupling. But if we don’t follow through with equities in Q4, then we know that time for decoupling is here and more aggressive buying could occur.

Developed nations with largest debts on record - Japan, but UK, EU, China et al are all on path to YCC - Yield Curve Control. No one explains this better than our own Arthur Hayes in Contagion. This means inflation is here to stay in these countries and their currencies will deteriorate further.

This is very bullish for USD, Gold and BTC in the longer term. This, in turn, is very bullish for the entire crypto ecosystem as builders counting to build and funders continuing to fund some amazing projects. My aim here is to find those opportunities and share them with you to the best of my abilities.

I am more positive now than last month. I believe that there is a very strong support around the 17.4K level for BTC. With most of the leverage in the system evaporated in the July crash, we could see some relief in coming months with a rally towards 24.5K by December. Current market is still a no trading zone and very apt for swing traders, BUT we could soon reverse if and when FED signals a pause. I am not expecting an overnight swing back to 60K, but trying to maximise opportunities that can maximise our return.

ETH is one such opportunity. A successful merge narrative was subdued by a moribund September macro. But with nearly 90% reduction in supply (equivalent to triple BTC halving), almost $400mn per month of miner selling pressure that just vanished, still the strongest DApp activity, L2’s and forks and integrations, all helping the cause - one has to bullish ETH in medium to long term. You can accumulate via options or DCA at these levels. This is not not financial advise but I like DCA the best. Or you could talk to Rising Cap and see if we can be of any help.

MAJOR ALTCOINS

COSMOS ecosystem got a huge boost with Atom 2.0 tokenomics. I have been eyeing the entire ecosystem very closely for the last 8 months now and have been generally bullish. I have been waiting on sidelines as markets crashed but now seems to be a good time to DCA or accumulate spot. Lot of projects are building on the Cosmos chain - games, bridges, stablecoins, other EVM chains on top like berachain or even EVM compatibility infrastructure like what Nitro labs is building.

$MATIC & $SOL- Polygon / Matic are constantly delivering amazing partnerships, great hires, new technology advancements like Zk rollups and a great push on NFT, Web 3.0 gaming and metaverse narrative by Polygon Studios. However, I am still looking for that killer DApp on Polygon to be honest. That could be there soon. $Solana is also consistently growing but not as aggressive as Polygon. They seem to be playing a larger game in the West with the announcement of a phone and a greater push in India via the SuperteamDAO. At $30-$35, I believe this is a good time to start DCA back with our base macro view in mind.

ALTCOINS mental model for Q4- What’s next: With sticky inflation and shaky macro, we might not see sustained rallies like 2020/21 in crypto but that does not mean, there won’t be opportunities . You just have to be more patient. Beware of merchants, influencers, traders and fund managers selling you overnight rags to riches stories. That said, where are these opportunities? Let’s explore:

L1’s: New L1’s like Aptos, Sui, Shardeum, Sei, Layer Zero etc would find it difficult to be the next Sol or Matic or Avax given their already inflated valuation (I’ve heard 8 bn valuations for some pre-product). But some of the new L1’s could still be a 10X opportunity. One can get some early access tokens by building projects, ecosystems or services around these new L1’s. For example there is this DEX on Aptos - Carbo Swap or other projects like Cetus Tsunami, Ferrum, Meta, Oracle etc. I am in no way associated with these but I am happy to brainstorm how I am going to be or how I will be positioning for these new L1 plays. The team is always trying to find early projects building on these new infrastructure and how to get involved with the entire ecosystem. Nothing is guaranteed, and at these huge valuations its difficult to be a fan. But we are here to make best RoI for our investors. With so many newly raised funds and such strong market makers and VC’s behind them, they could all rise exponentially at some point.

L2’s & ZkSync Season: I think the narrative will soon start shifting to ZkSync as they launch main net next month. What did well in this bear market on L2’s, would probably do well on ZkSyncs. What are those next GMX or FOLD? Is there a new DEX or a Stablecoin or a yield generating product? Any new web3 gaming project like Axie or a community project like Doodles or APE?

Football Season - Dubai / Qatar are already going crazy: Lock the date - 22nd November. Remember the rule - buy the rumour, sell the news. It is a decent narrative one could get behind. My top pick is $CHZ for overall narrative with football clubs and $ALGO who recently announced a partnership with FIFA

Other interesting coins: This dip is a boon if you have constant cash flow sources. I have started to take some positions and believe that DCA won’t be a bad strategy here - although macro needs to hold. Don’t take my word for it. DYOR and please don’t be a degenerate to go all in:

$BNB / FTT - Safe, secure and gradually expanding. More BNB than FTT. Will not give mega returns but will protect your downside in a balanced portfolio

$GALA / APE / SAND are some of my favourites for gaming and metaverse play with upcoming APE staking, it could become a hot narrative by end of the month

$GMX / GNS / BTRFLY / CRV / FXS - continuing to accumulate for now for some real yield. CRVusd launching mod October I believe

$LDO / FOLD - for merge play on ETH

$GMX / MAGIC for Arbitrum play although time to start rotating to ZkSync ecosystem

and more……..

There are a few more and I would be writing a proper long form note on Q4 crypto narrative and how I believe we all degen can play this season. Happy to discuss and brainstorm more with anyone. You can reach me here on twitter. DM’s are open.

Or we continue to post a lot of alpha on our no shills telegram channel here

FINAL WORD FOR OCTOBER

We are still chasing a macro, that is largely driven by the FED. In turn, the FED is depending on taming inflation and wage growth via its tightening policies.

While Bitcoin tried to decouple from macro and equities in general this month, we do not believe that is an absolute case yet. There are too many intertwined economic uncertainties to get aggressively behind that thought. Base case remains for the FED to tighten less aggressively into December and perhaps pause at some point in Q1.

As far as crypto is concerned, there is a lot of spare cash around this time. Brilliant founders building some awesome projects and infrastructure. I have never been more bullish in my last 10 years in crypto. This macro decadence “shall also pass” and things will eventually get better for the long term. Selectively accumulating and starting to DCA into some coins is how I would position myself. Nothing could be more apt for a closing remark like the famous Warren Buffets quote:

Best investors are fearful when others are greedy, and greedy when others are fearful

- Warren Buffet

RISING CAP THESIS - Keeping it simple

We are macro investors driven by narratives that shape the world, and in turn what shapes crypto in the medium to long term. Right now we are very focused on infrastructure as we are back to a BUIDL phase. If you are a brilliant founder with an awesome project idea, do reach out to us at hello@risingcap.co

We stay diversified and ask ourselves everyday, and you must too.

What is the market cap that the entire industry can collectively achieve from here? 10X to $10-$20 trillion?

Where are the medium & long term opportunities?

What are the risks? How do we protect against those? Basically how do we keep our investors money safe?

How do we build Rising into one of the marquee digital asset firms?

The following make Rising a very compelling proposition vs a long only passive Bitcoin position:

Highly experienced team in crypto

One of the largest deal networks build over last 10 years

Resourcefulness for founders, not just passive investors

You can learn more with us by subscribing to our resources here: