Headwinds & Tailwinds- Rising Cap Macro & Crypto Monthly

Headwinds & Tailwinds- Rising Cap Macro & Crypto Monthly

Liquidity crunch, failing economic indicators, caution ahead, crypto fights back

I have been trying to get this newsletter out since last week. A tsunami of daily macro and crypto news is making me update it before I add the latest “Curry Masala” to it. SO here it is, before Gary goes berserk again

Quick note: if you have not read the previous monthly post where I laid out some basic macro ideas for this year, this could be helpful:

Crash Lending to Crash Landing - Rising Cap Monthly Macro & Crypto

First it was the debt ceiling fiasco, yes no, yes no and then finally yes. Then it was the SEC suing Binance & CZ. While it was all expected but a sudden report covering illegal securities exchange, tokens as securities, list of other tokens etc etc caught everyone offside as we prepare for summer holidays. While volumes were already down, longs were liquidated immediately.

If that as not enough, and to teach Coinbase a lesson, SEC decided to sue Coinbase as well and Brian Armstrong immediately went on offensive stating he will not hesitate to go to Supreme Court to fight this battle.

If you ask me the prod moment was that BTC & ETH almost shrugged this and are back up where they started before SEC made the Binance news. What does this mean? Here are few quick thoughts:

Smart money has already left US shores. They are trading elsewhere and cannot risk their freedom money

Repeated regulatory threats and now some action, has muted peiople’s response. Knee jerk reaction at first. As soon as some sense prevails that this is a long drawn battle either side could win (or settle most probably), markets are back up

Fact that 30+ other nations are gearing to regularise and clarify crypto regulations (see Coinbase video above)

We’ve been advocating for ETH vs BTC due to its resilience when it comes to decentralised usage and that displayed better strength in this fiasco. More on that later in crypto section

Builders and investors are also moving to Dubai, Singapore and HK. In fact, no one wants to touch US right now in crypto. There is no need to honestly as funds are setting up entities abroad and founders are moving to crypto friendly (or at last neutral) jurisdictions

If I was China, I would immediately make crypto trading easy in HK and regularise it. I am sure some country will take this opportunity to accelerate adoption

DEX’s & PERP DEX’s volumes are constantly exceeding centralized exchange volumes for a reason. That will continue to increase and we will see better UI/UX and more invocation in there. We are already seeing much more pitches there in DeFi at Rising Capital. Coinbase and Binance will loose volumes and assets for a while but they will set up shops elsewhere more quicker now

Given how we withstood this onslaught from SEC, I believe bottom is nearly in barring any macro liquidity squeeze. If crypto can endure this, and FTX and Luna and Celsius, and BlockFi and ……and still be at 25K, there is no other way but upside.

Only remaining FUDs are now Tether and Staking like LIDO or BTC sale by Mt Gox and US Govt. Do you really think that bothers the deigns? What matters is liquidity from here on. More on that below

I believe that as liquidity traps are unleashed again by FED, and as we approach halving as well as election year, 2024 - its only inwards and upwards from there.

Clarity over confidence

This has been my number one mantra for years. A second derivative of clarity is asking better questions. Simple, easy, specific asks.

Once you make it a habit to ask specific questions, with clarity, you have won 90% of the battle. Not only you become confident as you progress with better questions, but your understanding of the world around you also becomes clearer.

I seldom ask questions that I do not have answers to, as silly as they might sound to my friends, colleagues, project founders, investors, family - everyone. Sometimes embarrassing, but as long as I get clarity I am a satisfied soul.

That said, we are going to try a clear approach this month - Context, Observation, Impact, Next - the COIN APPROACH

Context - Post debt ceiling liquidity situation and general macro environment

Observation - How does liquidity behave as TGA is replenished?

Impact - Clarifying second and third order derivative effects of our Observation

Next - Macro summary for coming months, what does that mean for stocks and crypto

Big Macro Picture

Inflation is not gone away YET but it’s slowing. Disinflation as a theme is gaining momentum as ISM, labour costs, German CPI, South Korean CPI, China manufacturing allow down. BUT employment numbers are still stronger forcing FED to increase rates one more time at least IMO.

Debt Ceiling passed without a hitch - this is positive for the USD and for

treasuries (more issuance, less dollars to buy). Banks and private reserves will go down and could cause stress in the system. FED’s QE/QT reposes depends on the severity of that stress. Meanwhile, Economy is slowing down and there is a very high probability of recession in H2.

Medium to longer term - end of Q4 or beginning of next year, FED starts to cut rates - 1) Either because we are in massive reserve depletion, credit tightening and recession (Something breaks, hard landing) 2) OR inflation is close to FED’s target (Soft landing, but highly unlikely IMO). Either way, printer is going to be turned on soon next year which is also an election year.

Shorter Term - Summer and Q3 - With geopolitical situations, upcoming liquidity tightening and reduced M2 supply, stocks are skewed to the downside, along with other risk assets. The rally could still continue but liquidity pressures will keep any lid on escalated returns form hereon. That is, no major upside from these elevated levels for next few months IMO

In summary, cash is your best friend bar few of your favourite long (or short) positions for shorter term - earning you 5-6% risk free until printers are turned back on.

You can always find quick daily summaries and thoughts on our no nonsense channel on telegram. Everyone is invited. No paid walls. Strictly no shilling. Share alpha, make money.

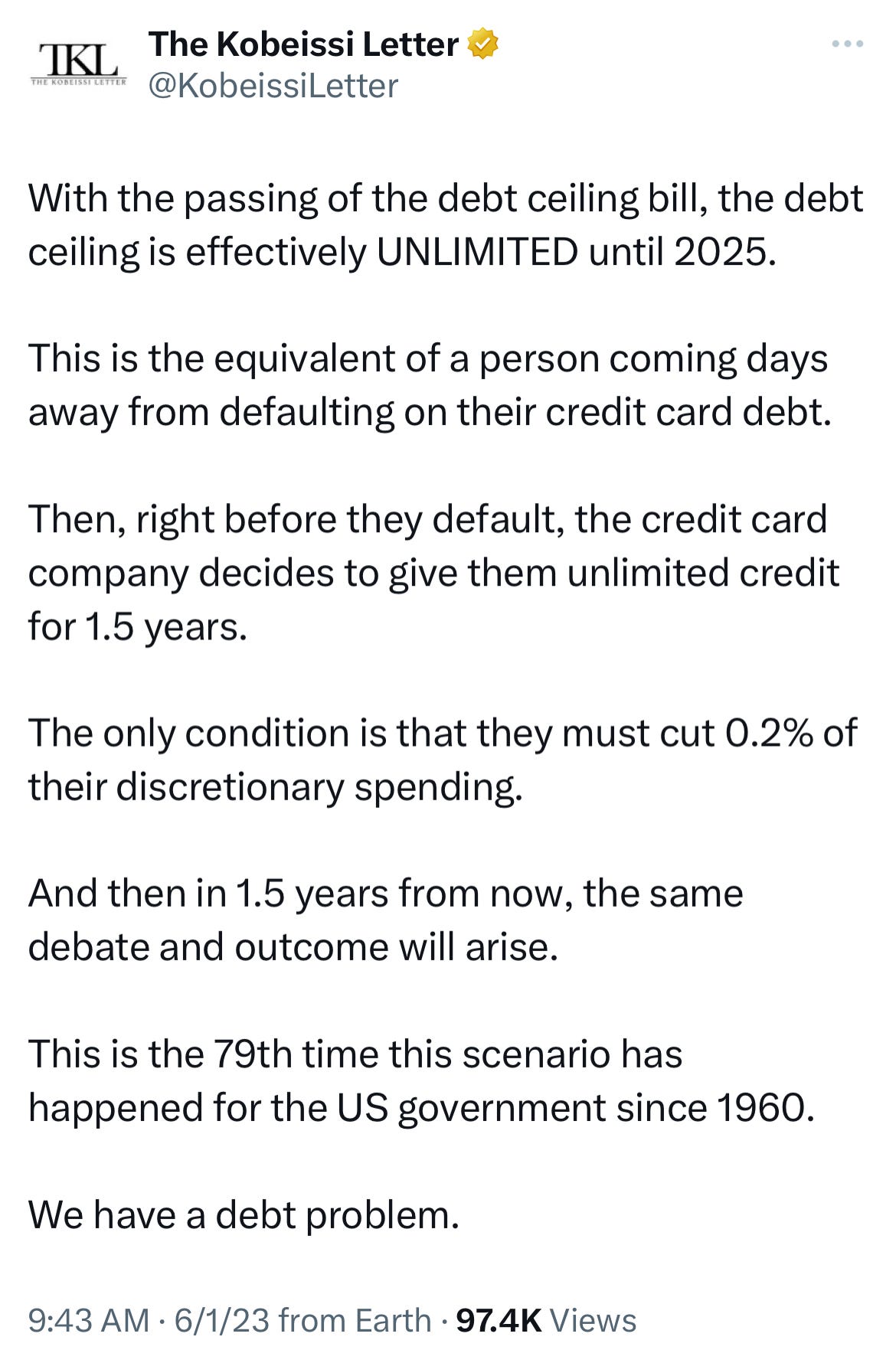

1. First a quick word on debt ceiling

The debt ceiling has been lifted for 2 years, with no limits

That means deficit spending is back on menu (already at $2 trillion plus)

This will add to the already whopping $32 trillion US National Debt

This spending will funded by money printing - i.e. higher inflation eventually

That also means higher rates for longer - higher mortgages, higher loans, higher everything costs

To sum it up - If your government is not cutting its’ spending, you will have to

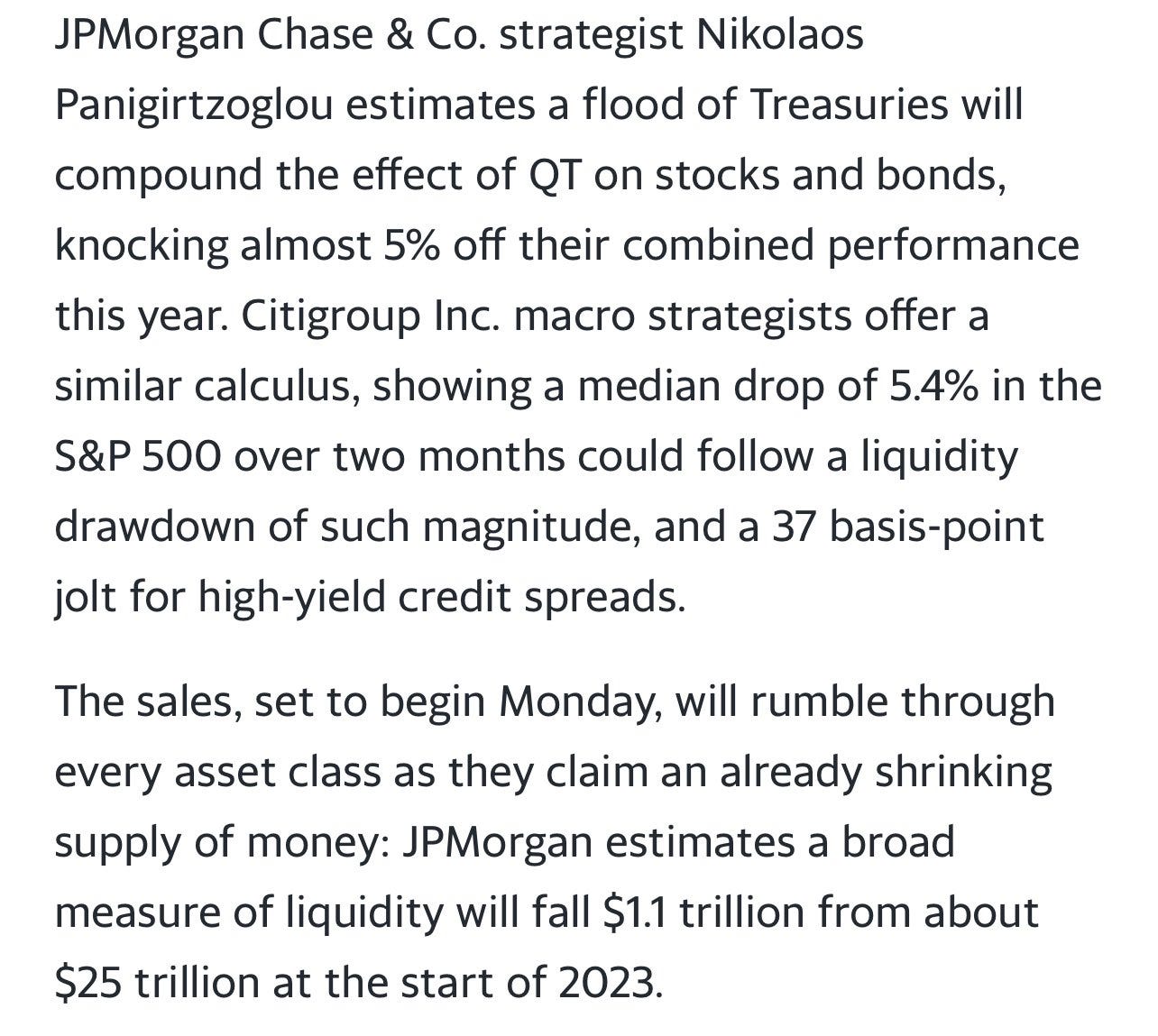

2. T-Bill Tsunami = Immediate Liquidity Crunch

TGA (Treasury General Accounts) are like governments checking account at the FED from which they pay daily, weekly and monthly bills. At around $30 billion, they are almost empty. Govt. needs to borrow ASAP to replenish TGA i.e. with an agreed higher debt ceiling limit, treasury will immediately flood the market with at least $500mn in T-bills. The big question is who will be the buyer of these TGA T-Bills?

By the end of Q3, that TGA refill number is expected to be greater than $1 trillion. This would drain even more liquidity, and raise lending rates, putting further pressure on US banking system. Yields should go up demanding more returns on their dollars. Consequently, USD goes higher as liquidity in dollars dries up

However, there is one piece of puzzle - FED’s reverse repurchase (RR) facility, where money-market funds park their cash with the FED overnight. Current rate is around 5% and around $2 Trillion is deposited there on an overnight basis. if TGA goes up, but repo goes down, then liquidity drain will be less.

However, I doubt if RR will go down significantly. In the end, everything depends on who is buying those TGA T-bills? My fear is banks will have to become forced buyers. If RR’s don’t come and buy some, that means bank deposits will be given up to replenish TGA. Which in turn means tighter liquidity. Stonks go down.

As cost of credit goes up, and dollar liquidity is tight, it starts to spread to other parts of economy. Lenders will demand higher rates as less dollars are available in the market (lower bond prices, higher yields). Cost of trading, cost of leveraging, cost of borrowing, everything goes up in the system. Or lenders don’t lend. Stocks go down again with stress in the system. I doubt if FED will pivot to QE unless something breaks. Keep and eye on that and load your trucks of cash to bread for that eventful day.

All in all, better liquidity situation in April & May that led to risk asset rally could flip in H2, leading to a possible correction in markets

3. Macro - Headwinds to Growth

Let’s see what data is telling us and try and position ourselves accordingly for next 3-6 months

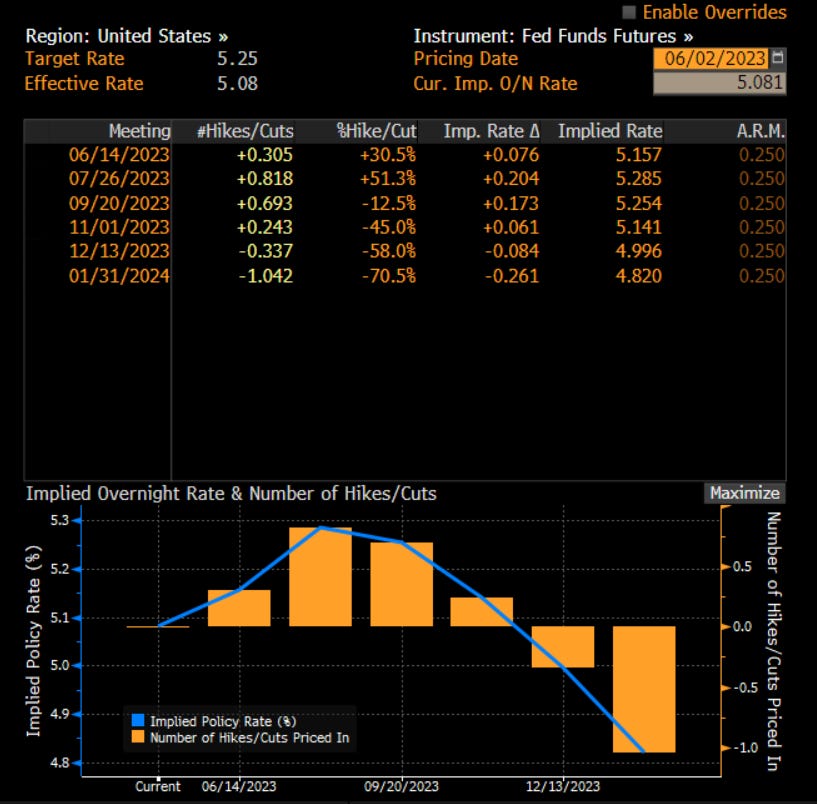

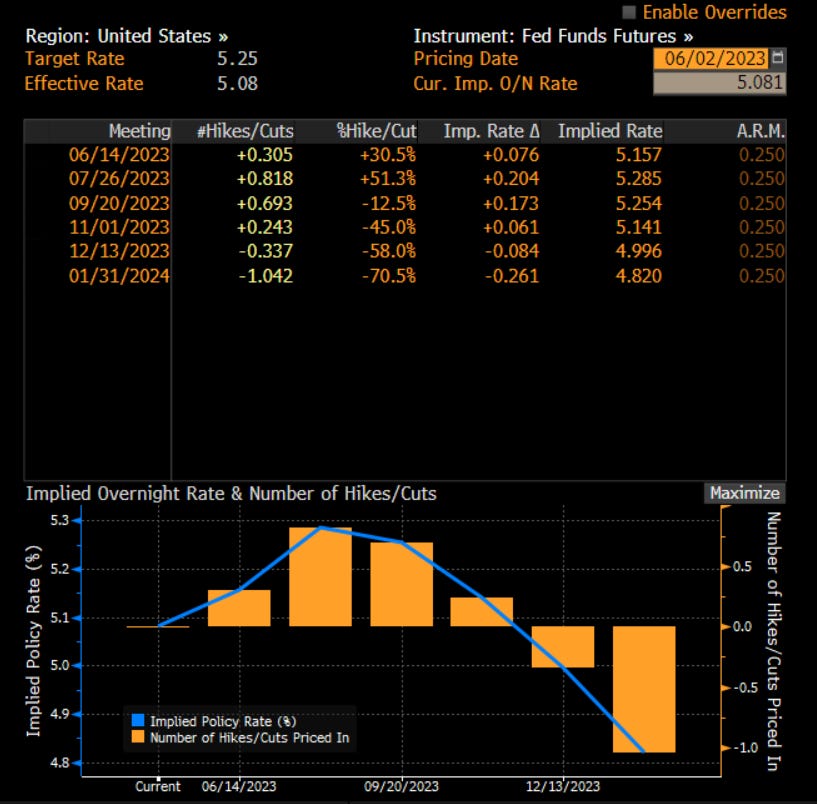

It is almost a 50:50 chance that FED will raise rates one more time on 14th June. However, market is pricing a cut by end of year. Till then, higher rates in H2, will continue to create tougher conditions everywhere in the system, not just banking. Something must break or inflation must come off drastically from here for FED to cut rates. But of you are patient, next year cuts are almost a given as election looms and boomer politicians do not want to take any drastic measure. IMO, stage is almost set for that. Ironically, the governement is almost hoping (or planning) that something breaks so that they have to loosen the rates quickly in 2024. Higher rates in H2, start cutitng in Q1 24’ and then looser further as election looms in.

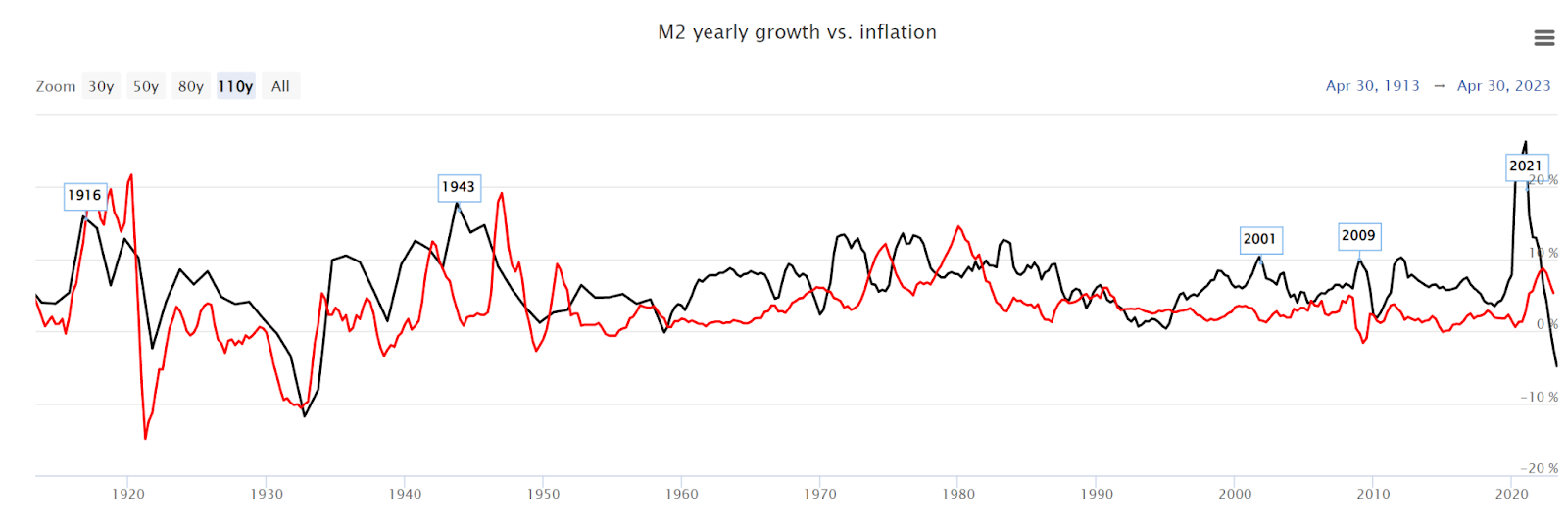

M2 money supply is most worrying though. Amount of money in the economy is falling by almost 5% every year. This is the fastest pace of money supply destruction since January of 1933. Lesser dollars in the system for now.

DXY should be higher in for next quarter amid tighter liquidity and declining money supply. China & Europe industrial numbers are already horrendous which does not bode well for EUR or CNH, against the mighty dollar

Inflation is not gone away YET but it’s slowing. Disinflation as a theme is gaining momentum as ISM, labour costs, German CPI, South Korean CPI, China manufacturing. BUT employment numbers are still stronger forcing FED to either increase rates one more time at least IMO.

Banking crisis has abated for now but still lurking in the background with threat of overnight failures and crisis escalating very quickly. No one is pulling that out

Tightening Bank Lending amid liquidity concerns, deteriorating conditions in their other portfolios like real estate and worsening macro conditions

Growth is contracting as consumers and corporate have to pay higher rates on loans, bonds, mortgages etc etc. Total credit card debt in the US has officially crossed $1 trillion for the first time in history, when average interest rates on credit card debt have hit a record high of 25%. The average American family now holds $10,000 in credit card debt, another record

War in Europe is getting extremely close to a larger blow up with tensions flaring up elsewhere as well

Arthur really sums up very well every time. We align. Link to the article and a summary if you click below.

MACRO SUMMARY

Declining M2, sticky inflation, rising consumer debt and higher rates for longer - does not bode well for the economy. As economy shrinks, we start to stare at deflation, and then recession.

Near term we could easily see a summer frenzy led by AI and positivity around debt ceiling resolution but as we enter Q3, things could get tighter, much tighter leading to a hard landing in H2

Longer term, we have an election year next year. Taps of liquidity will be opened again - back up your cash trucks for end of Q4/Q1 24’

Crypto Macro & Micro

Before Gary came barging in, crypto was already struggling in a range without institutional liquidity. That liquidity is expected to get tighter in H2 (see above in Macro). As such, there is a little more downside, albeit very limited, in coming months in crypto. Furthermore, crypto held very well with this SEC onslaught and makes me even more confident. As far as institutions are concerned, money market funds and QQQ are more attractive right now vs crypto. It was crypto all these years, it’s AI for now. And government bonds. Smart money will come back next year.

Bitcoin = Macro Liquidity + Network Effects

Macro Liquidity = Govt driven policies and rates + Arbitrage vs other asset classes

Network Effects = Technological advances + larger user base

Almost non existent volume in May, that was lowest in last few years barring April 22. Wallets and network grew due to ordinals but that was tiny winy micro payments. Hardly any buying or trading happening that excites us.

The biggest reason for lack of this aneimic volume is lack of institutional participation. Retail can buy spot and only carry it forward that much. At some point you need institutions that have been absent because:

Post FTX trauma and massive hit due to lenders like BlockFi, Celsius, FTX etc continue to haunt them. Most cases have still not reached their settlement

Regulatory overhang and no one wants to get caught in Gary’s cross hairs

Closure of major fiat on-off ramps delaying “effective” market making and rapid settlements

Higher rates elsewhere offering risk free 5% plus

AI driven mega stock rally - that has provided equivalent returns to institutional investors with much lesser risks

Pricewise, BTC has been consolidating between 29K to 25K for sometime now. We could see more pull backs as liquidity is drained by macro TGA replenishes, but my take is that it will be healthy, At a price between 20K to 25K, institutions will start to come back and could possibly lead to another rally as excess leverage gets drained. Assuming of course that macro plays along.

More institutional capital and some new narratives are needed for BTC to break 30K range. But there is a solid support at 25K and institutions step in at 20K. With the macro picture painted above for H2, I am of the view that institutions are happy making 5% -10% risk free. We could be headed towards 20K in H2 and those are the dips you do not want to miss for upcoming taps of liquidity in 2024.

BTC Summary

Just like May, June looks likely to be subdued. Volumes will continue to be low, as tourists travel for summer. And now we also have the Gary effect. While $20K looks unlikely, but if I’ve learned anything, never say never in crypto. Any dips below 25K are a buy but remember if there is a dinosaur extinction level macro event, nothing is ruled out. Fun, no?

On the upside, one things clear, no bull run till institutions come back. I don’t think they are coming back till they see clear signs of FED rates reversal. Not just a pause. Current risk free rates are attractive enough for them with current geopolitical risks around. But when they come, they move in sizes.

ETH = A Perpetual Bond with Infinite Applications

I have some very simple theories around ETH which make it a better investment against BTC in the long run. One cannot NOT have BTC in your portfolio, but ETH weightage should be a tad higher for the following reasons:

Post PoS ETH is a decentralised perpetual bond. As FED starts to decrease rates, institutions that are looking for a safe risk free 5%, will all flock to ETH. But first a majority of them will flock to BTCm and then ETH. Then alts. Decentralised ETH staking becomes very important in such scenarios

ETH is deflationary - supply < demand. As simple as that.

Most Apps are on ETH and most L2’s are EVM complaint (ETHEREUM Virtual Machine), always creating demand for ETH

For those simple reasons, I think ETHBTC will do very well, but in 2024, when institutional liquidity comes back.

Alts = Narrative - where are thou?

Without any clear narrative, alts are dumping hard. And some levels are starting to look attractive. Let’s see a few that I am personally watching. As usual DYOR, NFA, read disclaimer at the end.

SOL looks more attractive than ETH & BTC but if BTC goes to $20K, SOL could easily go to $15. That would be a very attractive level to grab all three.

Memecoins main seems to have settled, while some meme coins continue to pump and dump. I wouldn’t be touching them for now. We made a good call in our last newsletter and exited almost at peak. Thank you very much.

BRC-20 tokens and the projects around it are getting all the funding these days. Inscriptions and ordinals have been making waves with BRC-20 market cap surging to around $600m, led by $ORDI token (a BRC-20 and not the actual ordinals) with a trading volume of > $200mn. But at the same time, this is cluttering BTC narrative.

“What if I tokenize all of the stocks and ETFs trading on NASDAQ so individuals can take personal custody of their shares of stock instead of leaving them locked up with a centralized custodian?”

- Microstrategy’s Michael Saylor

Chinese coins are becoming hotter as China / HK here looking to re-open. Not sure how much of this resurgence is true, but would not be a bad trade to hold some Chian narrative tokens - TRON, Conflux, Nucleon and Elastos. HK has allowed licensed trading platform operators to service retail investors from June 1, 2023.

Liquid staking narrative is also back including new projects like Prisma and older protocols like BTRFLY, Pendle etc.

Other narratives to watch this summer

RWAs (asset management protocols, decentralised treasuries

Decentralized data and storage-oriented blockchains like Filecoin and Kyve

New L1’s like Eigenlayer, Mantle as well as Berachain, an EVM-compatible L1 blockchain built on the Cosmos SDK

Crypto Narratives Displayer very nicely on Dune by CryptoKoryo. Click below

Lastly - Some Interesting Content

Apple VR Headsets - Beginning of a new Era

Karen Karniol-Tambour, Co-CIO at Bridgewater Associates talk Macro